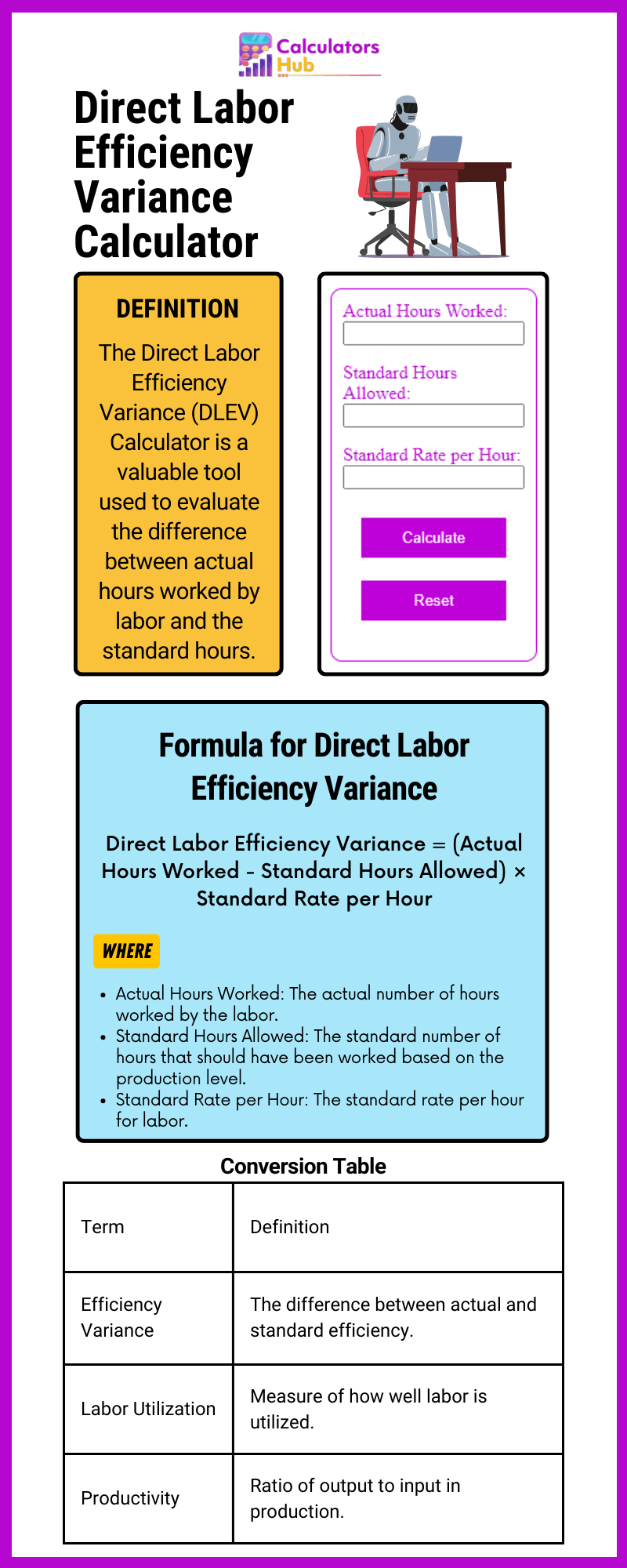

Direct Labor Variances Formula, Types, Calculation, Examples

Addressing these challenges requires a comprehensive approach involving continuous evaluation, industry foresight, and a nuanced understanding of the production landscape. During the year, the company spends 200,000 hours producing 35,000 of output. Calculating DLYV is important to assess the productivity of labor and identify areas where operational efficiency can be improved. Efficiency variance calculations not only apply to the output of tangible goods, but they also apply to the completion of cerebral tasks, such as the number of hours it takes to audit an individual’s tax records.

Causes of direct labor efficiency variance

The unfavorable variance tells the management to look at the production process and identify where the loopholes are, and how to fix them. Labor efficiency variance compares the actual direct labor and estimated direct labor for units produced during the period. Conversely, when the calculation yields a positive number, it demonstrates an unfavorable variance and shows that the work was done inefficiently. When you apply the formula to financial accounting, you get meaningful results at a glance.

ACCA PM Syllabus D. Budgeting And Control – Labour total, rate and efficiency variance – Notes 2 / 5

If the number is negative, then it reflects a cost savings over your expectations. By convention, the negative sign is usually dropped, and the word “favorable” is attached to the variance instead. The combination of the two variances can produce one overall total direct labor cost variance. If the outcome is unfavorable, the actual costs related to labor were more than the expected (standard) costs.

AccountingTools

A positive variance signals higher efficiency, contrasting a negative variance that suggests lower productivity than projected. In this case, the actual hours worked are \(0.05\) per box, the standard hours are \(0.10\) per box, and the standard rate per hour is \(\$8.00\). This is a favorable outcome because the actual hours worked were less than the standard hours expected. As a result of this favorable outcome information, the company may consider continuing operations as they exist, or could change future budget projections to reflect higher profit margins, among other things.

What does the direct labor efficiency variance tell us?

- Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications.

- Since the baseline theoretical inputs are often calculated for the optimal conditions, a slightly negative efficiency variance is normally expected.

- During the year, the company spends 200,000 hours producing 35,000 of output.

- Direct labor variance is a means to mathematically compare expected labor costs to actual labor costs.

Labor rate variance measures the difference between the actual and standard labor rates, highlighting cost fluctuations due to wage variations. On the other hand, LEV gauges the variance arising from differences in actual and standard hours worked, focusing on productivity changes. Essentially, labor rate variance addresses wage-related costs, while labor efficiency variance assesses the impact of productivity variations on labor costs. The purpose of calculating the direct labor efficiency variance is to measure the performance of the production department in utilizing the abilities of the workers.

Why You Can Trust Finance Strategists

The direct labour rate variance is the difference between the standard cost and the actual cost for the actual number of hours paid for. Possible causes of an unfavorable efficiency variance include poorly trained workers, poor quality materials, faulty equipment, and poor supervision. Another important reason of an unfavorable labor efficiency variance may be insufficient file w2 online demand for company’s products. Before we go on to explore the variances related to indirect costs (manufacturing overhead), check your understanding of the direct labor efficiency variance. Use the following information to calculate direct labor efficiency variance. This formula gives you a clear picture of how much the actual labor usage deviated from the budgeted amount.

If the company fails to control the efficiency of labor, then it becomes very difficult for the company to survive in the market. The management estimate that 2000 hours should be used for packing 1000 kinds of cotton or glass. It is a very important tool for management as it provides the management with a very close look at the efficiency of labor work. When you make the most of variance analysis, you can quickly find efficiency problems and resolve them.

The same calculation is shown as follows using the outcomes of the direct labor rate and time variances. If the actual hours worked are less than the standard hours at the actual production output level, the variance will be a favorable variance. A favorable outcome means you used fewer hours than anticipated to make the actual number of production units. If, however, the actual hours worked are greater than the standard hours at the actual production output level, the variance will be unfavorable. An unfavorable outcome means you used more hours than anticipated to make the actual number of production units.

This figure can vary considerably, based on assumptions regarding the setup time of a production run, the availability of materials and machine capacity, employee skill levels, the duration of a production run, and other factors. Thus, the multitude of variables involved makes it especially difficult to create a standard that you can meaningfully compare to actual results. It occurs when the actual hours worked are more than the standard hours allotted for a specific level of production. In such cases, the negative variance indicates lower efficiency, as more time than expected was needed to complete the work. Doctors, for example, have a time allotment for a physical exam and base their fee on the expected time.